Yes Bank Crisis and Reconstruction: Explained

Yes Bank Crisis and Reconstruction: Explained

What is YES Bank Crisis? Is the YES bank crisis over? Is the depositors’ money in the YES Bank safe? What is the reconstruction scheme of YES Bank proposed by RBI? Read this post to understand the YES Bank story in detail.

What is YES Bank Crisis? Is the YES bank crisis over? Is the depositors’ money in the YES Bank safe? What is the reconstruction scheme of YES Bank proposed by RBI? Read this post to understand the YES Bank story in detail.

Banks play a pivotal role in the economic growth of the country. Failure of a bank, irrespective of the ownership, private sector or public sector, can impact everyone. Hence, neither Government of India nor Reserve Bank of India (RBI) never lets a bank – facing troubles in its financial position – to fail.

Yes Bank Ltd, one of the major private banks in India, has been facing the problem of rapidly deteriorating financial position. This necessitated Reserve Bank of India (RBI) to take immediate action in the form of a reconstruction scheme to protect depositors money.

YES Bank History

Yes Bank, started in 2004, is one of the new generation private banks that were allowed to start banking operations by Reserve Bank of India in the post-liberalisation era. The bank was founded by Rana Kapoor and Ashok Kapur.

The bank engaged in highrisk lending, providing loans to those who could not raise funds elsewhere.

The assets books of Yes bank showed promising growth until 2017 when the problem of Non-Performing Assets (NPAs) came into the highlight.

How big is YES Bank?

YES bank is currently India’s fifth-largest private sector lender.

Yes bank had deposits of Rs. 2 lakh crore. Its total assets including loans given are Rs.3.5 lakh crore.

The bank has 18000+ employees and has more than 1100 branches and 1300 ATMs.

YES Bank Crisis

Loans not repaid is a major issue of most banks in India. These bad loans are called Non-Performing Assets (NPA). The Gross Non-Performing Assets of YES Bank was 7.4% of the gross advances at the end of September 2019. It became 18.87 per cent of the bank’s total loan book (or Rs 40,709.20 crore) at the end of December 2019.

The crisis at YES Bank started when the huge NPA issue at YES Bank became public.

For the quarter ended December 2019, Yes Bank reported a loss of Rs 18,564 crore compared to a profit of Rs 1001 crore in the same quarter in 2018. The bank’s net loss would have been wider at Rs 24,778 crore in the third quarter if it weren’t for a tax write-back of Rs 6,214 crore. In the preceding quarter, Yes Bank had reported a net loss of Rs 600 crore.

Bad loans

The founder Rana Kapoor had personal connections with most of the high-level industrialists who sought his help for loans, which went not repaid. Some of the big defaulters to whom the bank had advanced funds included IL&FS, Anil Ambani group, CG Power, Cox & Kings, Café Coffee Day, Essel group, Essar Power, Vardaraj Cement, Radius Developers, and Mantri Group.

The Bad loans of Yes Bank are estimated to be around Rs.40000 crore (Gross NPA). While the Gross NPA was around 19% of advances, Net NPA was around 6% of loans at the end of December 2019.

Eroded capital base

The overall capital adequacy ratio dropped to 4.2 per cent from 16.3 per cent in the preceding quarter.

The capital base – specifically the Core Equity Tier-1 ratio – fell to 0.6 per cent at the end of the quarter compared to 8.7 per cent in the September quarter. The minimum regulatory requirement stands at 7.375 per cent.

Breach of RBI mandated ratios

YES bank’s statutory liquidity ratio has breached the RBI’s minimum requirement and so has its liquidity coverage ratio. The bank has thus provided Rs 86 crore as a penalty to the central bank.

Governance Issue: Under-reporting of NPAs

It is not just that Yes Bank had NPAs, but it under-reported NPAs which was later found out by RBI. This led to the end of the tenure of the founder Rana Kapoor as the CEO (2018).

Deposits vs Loans

In the last five years, the loan book grew by over four times, but deposits failed to keep pace with loan growth. The loan book grew to ₹2,24,505 crore as of September 2019, while deposits were at only at ₹2,09,497 crore.

Unusual increase in loans given from FY 2014 – FY 2019

As per news reports, the loan book of Yes Bank had grown from Rs. 55,000 crore in FY 2014 to Rs. 2,41,000 core in FY 2019. When overall bank credit during the above period grew only by about 10 per cent, it unusual to notice that YES Bank’s loan book grow by about 35 per cent.

Rumours spread through social media

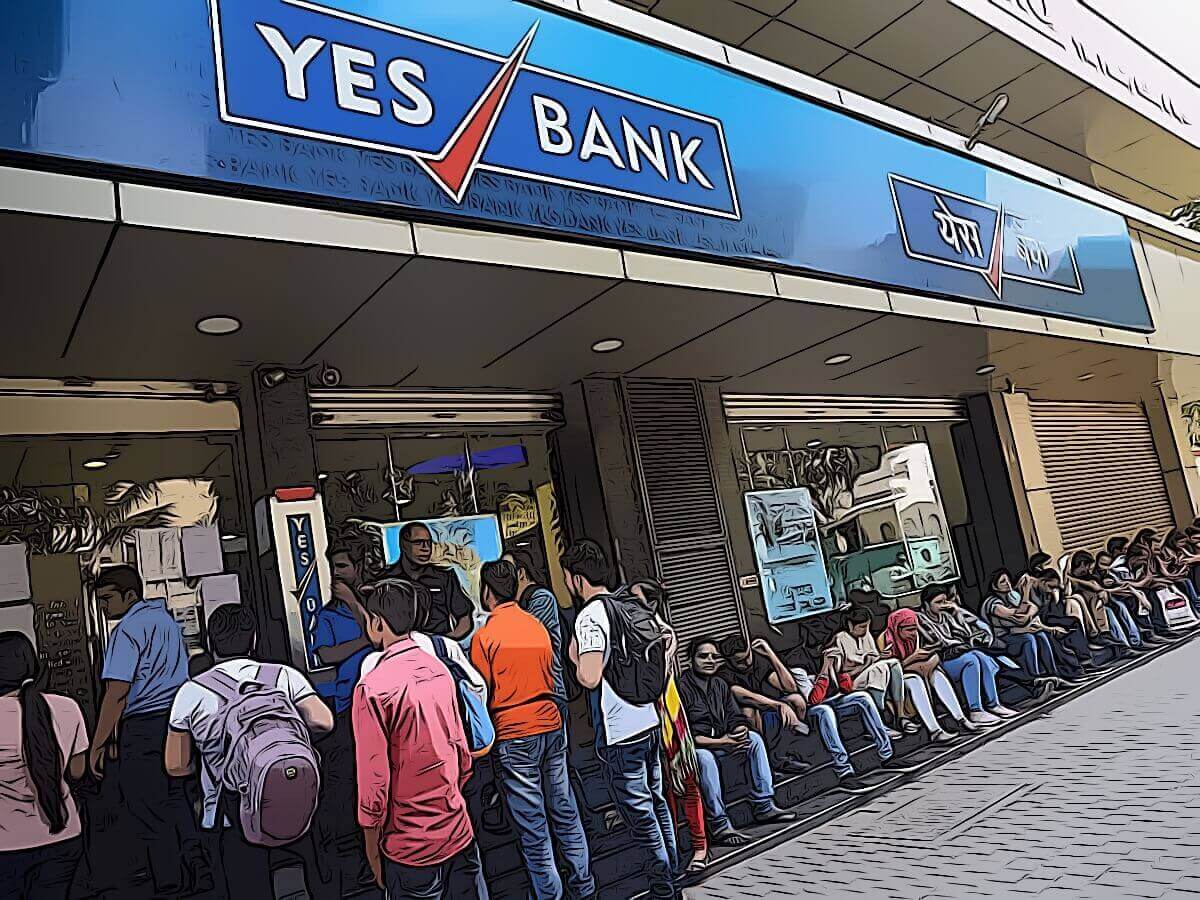

Rumours spread through social media about the possible collapse of Yes Bank when it was capable of managing its balance sheet, added fuel to the fire. Many false news and rumours resulted in shrinking of the deposit base of YES bank.

As on Dec. 31, 2019, the bank’s outstanding deposit base stood reduced to 1.65 lakh crore from Rs 2.09 lakh crore on Sep. 30, 2019. The lender continues to see an outflow of deposits since Dec. 31; its total deposits stood at Rs 1.37 lakh crore, as on Mar. 5.

The bank’s failure to raise fresh capital

As the bank had a lot of bad loans (in the tune of Rs.10,000+ crore), it needed fresh capital to manage its operations. The bank’s failure to raise capital led to rating downgrades, which made capital-raising even more difficult.

RBI moratorium

All the above factors led the RBI to conclude that there was no “credible revival plan” from the end of YES bank and so “in the public interest and the interest of the bank’s depositors” there was “no alternative” but to place the bank under a moratorium.

RBI to took over from YES bank board for 30 days. The central bank has appointed deputy managing director and chief finance officer of State Bank of India, Prashant Kumar, as an administrator of the bank.

The Central Bank of India then imposed limits on withdrawals to protect depositors.

Reserve Bank of India under Sub-section (1) of Section 45 of the Banking Regulation Act, 1949, the Government of India has made an Order of Moratorium in respect of Yes Bank Ltd. under Sub-section (2) of the said Section for the period from 5th day of March 2020 and up to and inclusive of the 3rd day of April 2020.

Yes Bank Ltd. Reconstruction Scheme, 2020

Reserve Bank of India (RBI) stated that State Bank of India (SBI) has expressed its willingness to make an investment in Yes Bank Ltd. and participate in its reconstruction scheme. Therefore, as per the of the powers conferred by sub-section (4) of section 45 of the Banking Regulation Act, 1949, the Reserve Bank of India, proposed the details of the scheme for raising fresh capital for Yes Bank.

The authorised capital of the Reconstructed bank

As per the government notification, the Authorised Capital of the Reconstructed Yes Bank shall stand altered to Rs. 6200 crore from the Rs.1100 crore earlier. The number of equity shares will stand altered to 3000 crore. The capital of the reconstructed bank at Rs.2 face value per share would be Rs. 6000 crores.

Authorised preference share capital shall continue to be Rs 200 crore.

How much should the investor bank invest?

The investor bank (Eg: SBI) can purchase up to 49% in the reconstructed YES bank. The investor bank should purchase each share at price not less than Rs.10 (ie at a premium of Rs.8).

So, if SBI is purchasing 49% of 3000 crore YES Bank shares at Rs.10 per share, that would mean it will be investing Rs.14700 crores to purchase 1470 crore shares of the private bank. SBI had approved an investment of Rs 7,250 crore in Yes Bank by purchasing 725 crore equity shares.

PS: The Main Investor bank (SBI) is not allowed to reduce its holding below 26% before completion of three years from the date of infusion of the capital.

New Investors in YES Bank

Apart from SBI, YES Bank got a lot of new investors as well.

ICICI Bank and Housing Development Finance Corporation Ltd announced that they will be investing Rs 1,000 crore each in Yes Bank’s equity. Axis Bank and Kotak Mahindra Bank will be investing Rs 600 crore and Rs 500 crore respectively. Bandhan Bank will be investing Rs 300 crore.

Existing shareholders own 255 crore shares, and they will end up with a roughly 8.5% stake in the company.

The balance 41.5% stake will presumably be held by other institutions and investors, who will need to infuse roughly ₹ 12450 crores, assuming the acquisition price is ₹ 10 per share.

Expected total new investment in YES Bank

The total new investment expected in YES bank in the near future from SBI and other investors in the company is expected to be at least Rs.27150 crore.

Writing down of AT-1 bonds

In a separate disclosure made to exchanges, Yes Bank said that the additional tier-1 bonds issued by the lender would need to be written down since the bank has reached the ‘point of non-viability’ trigger.

As per Basel rules, AT-1 bonds are loss-absorbing capital instruments and should be written down when a bank breaches certain thresholds of core equity tier-1 capital.

The bank has Rs 8,415 crore in such bonds outstanding.

Is the new deal a merger of YES Bank with SBI?

No.

The current deal is not a merger with SBI rather an equity investment by SBI in YES BANK.

PS: Merger with SBI is also a promising deal for YES Bank and its depositors. However, the merger of the private bank with the state bank is something which would be worked out only if the current investment deal does not bring the desired results.

Will YES Bank be shut down?

No.

The government or RBI has no plans to do that. The deal is not even a merger scheme, but a plan to revive the private bank to its old glory.

Is the Yes Bank Crisis over?

Hopefully yes, if the reconstruction scheme is properly implemented.

From the depositors perspective, their hard-earned money may get locked up for a few more weeks. However, as assured by the Finance Minister, their deposits will be protected.

Once the reconstructed bank resumes its operations, and gets backs the loans given, gradually YES bank may be back to normal. All we can do now is to wait and watch.

YES Bank-SBI Deal

SBI board has given in-principle approval of exploring the possibility of picking up a stake of up to 49 per cent in Yes Bank. The draft plan is out. However, the deal is not finalised yet.

The best possible Scheme for the reconstruction of YES Bank

The SBI investment in Yes Bank is the best deal the capital-thirsty private bank can ask for. The presence of a credible name like SBI is very important for a resolution.

If the deal goes as per plan, depositors of YES Bank are in safe hands and have nothing to worry about. The survival of YES Bank is critical to preventing a contagion in the banking industry.

Rajnish Kumar, SBI chairman sounded confident of implementing the restructuring proposal for YES Bank before the 30-day RBI imposed moratorium period ends. Once YES Bank was out of moratorium it would be run by a professional team.

Main Stake Holders

- Depositors in YES Bank

- Investors in YES Bank (shareholders)

- Investors in SBI (shareholders)

The primary objective of RBI or government in a crisis like that of YES Bank is to safeguard the hard-earned money of depositors. RBI assured depositors of the bank that their interests will be fully protected and there is no need to panic.

The next priority is to safeguard the interest of investors (shareholders), however, this does not seem to be easy.

Yes bank’s shareholders would surely be the biggest losers. Going by the experience of banks placed under moratorium earlier by RBI, shareholders are unlikely to be compensated.

Shares of Yes Bank, which traded at 404 rupees at its peak in August 2019, fell to a record low of 5.65 rupees on March 2020, with the stock plunging nearly 85%.

Most of the shareholders of YES bank will be happy to see a credible investor like SBI investing heavily in YES Bank. However, the shareholders of SBI is worried about the top public sector bank’s investment in a loss-making private bank, which may not give any immediate returns.

The issue of conflict of interest in SBI Investment in Yes Bank

Will there be a conflict of interest when a public sector bank invests in a private sector bank? Will the SBI pull-out customers of Yes Bank into its database? Will deposits move out from YES Bank to SBI.

SBI chairman believes that there is no conflict of interest.

The plan is to keep YES Bank and SBI separate, leaving scope for the state-run lender to exit the investment when YES bank turns profitable.

Though the new board of Yes Bank will be constituted with two nominees from SBI to build the trust of investors and depositors, SBI management would not be involved in the day-to-day management of the private lender.

The solution for YES Bank Crisis

SBI should take over the loan book of YES Bank, recover the loans, and return the depositors money.

The new draft scheme proposes full repayment of all deposits, dilution of equity, and write-off of Rs 10,800 crore of additional tier one (AT-1) bonds.

YES Bank and RBI

The Reserve Bank of India (RBI) already facing criticism on major supervision lapses in cases like Punjab National Bank (PNB) and Punjab and Maharashtra Cooperative Bank (PMC), couldn’t have afforded Yes Bank to fail.

Yes Bank Crisis: Why RBI missed seeing the signs?

Reserve Bank of India did notice pressure points as early as 2017, which eventually led to the regulator denying extension to the then MD & CEO Rana Kapoor, despite the board’s endorsement.

However, RBI failed to come up with a concrete step like pooling SBI into the scheme of things until things became worse.

If the government and RBI acted earlier, they could have gained the confidence of depositors and retained much of the money. Also, the painful steps like moratorium and restriction on the withdrawal – which results in the loss of people’s confidence in the economy – could have been avoided if they acted earlier.

Yes Bank Crisis: It is time to reform RBI?

RBI is burdened with too many responsibilities.

The government must reduce the RBI’s responsibilities so that the central bank can focus on the key areas.

A few suggestions: The securities regulation should move to the Securities and Exchange Board of India (SEBI); debt management should be given to an independent debt management agency, and infrastructure systems operated by RBI should be corporatised.

As mentioned before, a specialised independent mechanism (resolution authority) should be directly monitoring the performance issues of banks like Yes Bank. Most of the G-20 countries have built specialised capabilities to resolve failed financial firms. Such a mechanism can keep a check on the regulator’s tendency to delay recognition of failure, thereby ensuring quick and orderly resolution.

Wilful Default vs Non-Wilful Default

Bank robbery is an initiative of amateurs. True professionals establish a bank. — Bertolt Brecht.

The government and RBI should analyse the default in the case of loans taken by corporates is willful or not.

If it is wilful, a detailed investigation should be done regarding the background of the tie-ups between Yes Bank and its corporate clients. An enquiry should be conducted regarding indiscriminate lending and fund usage in the last 3 years – when the investment climate was utterly gloomy that only a few genuine companies were seeking loans for fresh investment.

If it is not wilful, the root cause lies in the pain points in the economy which should be identified and corrected.

Bank Crisis and Bailouts in India

The bailout is the act of giving financial assistance to a failing business to save it from collapse.

In India, how many banks have failed?

In India, no scheduled commercial bank has been allowed to collapse (or fail) since 1991.

The central bank and the government have always made sure that a failing bank gets acquired before it drowns.

Only cooperative banks have failed here. As per figures from the Deposit Insurance and Credit Guarantee Corporation (DICGC), authority that provides deposit insurance in the country, the cases of about 350 such banks have been settled so far for a payout of Rs 4,822 crore in claims.

RBI will not allow any scheduled commercial bank to fail

In India, most of the scheduled commercial banks are considered entities which are ‘too big to fail’.

A previous example is the case of Global Trust Bank. Global Trust Bank was merged with Oriental Bank of Commerce to avoid failure.

Depositors will not lose money

Finance Minister Nirmala Sitharaman, RBI governor Shaktikanta Das, and SBI chairman Rajnish Kumar had assured that the money of depositors will be safe.

In the recent past, there are no instances in India where depositors lost money in case of a scheduled bank collapse.

Moratorium by RBI and its impact

The market was enthusiastic with the news of SBI intervention as an investor in Yes Bank. However, the moratorium (temporary prohibition of an activity) and equity dilution plan shocked investors and depositors alike.

Probably the moratorium was needed to prevent further erosion of deposits because of any rumours or insider news.

Once the reconstructed YES bank starts functioning, the banking process should hopefully be back to normal. There might be a delay for depositors to get their money back, however, this should not mean losing any hard-earned money.

Private Bank vs Public Sector Bank: Which is safe?

Public Sector Banks have 51% or more of the government equity stake in it. However, with respect to the safety net of depositors, private banks and the public sector banks are almost the same.

If a bank fails, the maximum insurance amount is limited to Rs.5 lakh per account for both private bank and public sector bank.

However, be it a private or public sector bank, government and RBI would normally intervene much before the bank goes beyond redemption. The resolution may be in the form of additional equity or a merger with a stronger bank.

RBI norms to protect depositors from a bank collapse

Scheduled commercial banks include private banks and public sector banks. Both are supervised and regulated by RBI. They have the same norms as well.

They cannot lend the entire money that they have received from depositors: 4 per cent of these deposits has to be kept aside as cash reserve ratio (CRR) and 18.75 per cent as the statutory liquid ratio (SLR).

Also, these banks have to maintain adequate capital when compared with risky loans given. This requirement is known as the capital adequacy ratio (capital-to-risk weighted assets ratio [CRAR]). CRAR is currently at 9 per cent.

Has any bank of YES bank’s size failed in India in the past?

Apart from co-operative banks, no scheduled commercial bank in modern India has failed to result in loss of depositor money.

RBI has always stepped in to bail out ailing banks – often merging it with another stronger bank or infusing extra capital, and thus protecting the depositor money.

This is the first time the central bank has taken such drastic action like moratorium with respect to a big bank like Yes Bank.

A near similar instance was in July 2004 when the RBI got state-run Oriental Bank of Commerce to take over Global Trust Bank to rescue the private sector lender.

Recent Bank Bailouts

Recent examples:

- IDBI Bank Crisis – In 2018, the government got LIC to bail out IDBI Bank with a Rs 21,624 crore capital infusion.

- PNB Bank Crisis – In 2018, the government paid the scam-hit Punjab National Bank (PNB) Rs 2,816 crore as a capital infusion from the via a preferential allotment of equity shares.

- PMC Bank Crisis – In 2019, the Punjab & Maharashtra Co-operative Bank Limited was been put under restrictions by RBI, after an alleged Rs 4,355 crore scam came to light. PMC bank may be merged with Maharashtra State Cooperative (MSC) Bank in the near future.

Which will be the next bank that will be in crisis?

Nobody can be sure of any bank.

The balance sheets of other banks too may be inflated, like what happened with YES bank. Only an independent and efficient audit check can find out the real issues.

RBI needs to more cautious with the scrutiny of the balance sheet of private and public sector banks.

Is it a good idea to bail out private banks using taxpayers money?

In this case of reconstruction of Yes Bank, which is a private bank, the investment from State Bank of India (a public sector bank) will be used. Public Sector Banks like SBI has 51% government’s share – which is taxpayers money.

There are many who raise concerns in wasting taxpayers’ money to bail out failing private entities. This quick remedy of government’s indirect investment in private firms is also against the current principle of the State exiting from even public firms.

However, considering no other alternative now, this bailout should be seen as an exception rather than the rule.

Should RBI keep on bailing out ailing banks?

When the cost of not bailing out an ailing bank for the economy and banking system is far higher than bailing out, this looks to be the only option.

If a bank collapse ruining depositors money, the repercussions will be huge.

That will not be limited to the banking sector but will affect the economy as a whole. It will also have social and political ramifications.

Banking Sector Reforms

Indian Banking Sector is going through a tough time. It’s time for immediate reforms like the merger of banks, bank resolution authority etc. Also, the root cause of the NPA issue should be identified and properly addressed.

Proper Solution to the Twin Balance Sheet Problem (TBS)

Previous Economic Surveys of India had already talked about the twin balance sheet problem of India.

The problem of banks is often not a balance sheet problem at the bank’s end alone. It is also a problem of the corporates to which it gave loans.

Why are the corporates not repaying the loans-taken?

Every time, it may not be a wilful default.

The government policies, rules, regulations, or even Supreme Court judgments might be the bottle-necks for corporate houses to run a business smoothly, earn a profit, and repay the loan.

Deposit Insurance

India is one of the countries that offer the lowest protection to depositors in cases of a bank failure. Whatever be the deposit in the bank account, only deposits up to Rs.5 lakh is covered by deposit insurance. (Budget 2020)

Deposit Insurance should be increased further to increase trust in the banking system.

In India, deposit insurance is provided by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly-owned subsidiary of RBI. DICGC collects a premium of 0.05% on the entire outstanding deposit from banks (and not from depositors).

The need for a resolution authority

A Resolution Authority is needed to take over failing banks and either run them temporarily, sell them, infuse equity or, as a last resort, liquidate them.

FRDI Bill

Financial Resolution and Deposit Insurance (FRDI) Bill was introduced in Parliament in 2017 to create a Resolution Authority. Unfortunately, it got mired in controversy. To address concerns with the Bill, the Union Budget 2020-21 raised the deposit insurance cap to Rs 5 lakh.

The Finance Minister has subsequently announced that the FRDI Bill will be brought back to Parliament. The Yes Bank moratorium should help put the bill on a fast track.

Merger of Banks

To strengthen the Indian Banking sector, the Central Government of India has announced the merger of ten public sector banks into four banks.

After the merger of banks, the country will have 12 public sector banks instead of 27.

Conclusion

Yes Bank was one of the highest-rated new generation private banks until 2017 when the bank started to face serious bad loan issue.

To stabilise the bank, Yes Bank Ltd. Reconstruction Scheme, 2020 was introduced by the Reserve Bank of India. RBI had also imposed temporary restrictions regarding the withdrawal of deposits.

SBI board has given in-principle approval of exploring the possibility of picking up a stake of up to 49 per cent in Yes Bank. However, the deal is not finalised yet.

To protect the depositors, the bank must be quickly reconstructed. Also, steps should be taken to liquidate the NPAs. If Yes Bank is resolved effectively, it will protect Yes Bank’s depositors, and maintain trust in the entire banking system.

Post a Comment